The top-line results of the Association of Language Travel Organisations (ALTO)’s first Language Travel Industry Survey were presented recently to its members – language schools and education counselling companies – with overall buoyancy in business cited among both sets of stakeholders that took part.

News and business analysis for Professionals in International Education

Have some pie!

ALTO’s first Language Travel Industry Survey is upbeat

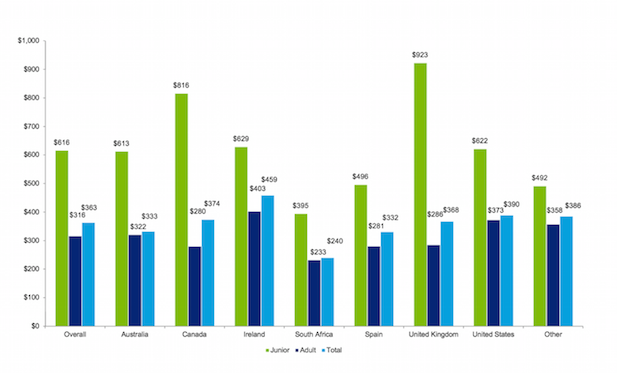

Average turnover per student week, according to the ALTO survey

Average turnover per student week, according to the ALTO survey This was the first attempt by ALTO and consultancy firm Deloitte to take a considered and anonymous pulse of the language travel industry and produce such detailed statistics about business performance and financial variables.

60% of providers surveyed indicated that they saw a rise in student weeks taught for adult learners in 2014 compared with 2013

The adult language travel market was reported to be growing overall. Sixty per cent of providers surveyed indicated that they saw a rise in student weeks taught for adult learners in 2014 compared with 2013, with growth averaging at 16%. For juniors, growth was also recorded at a lower but healthy 9% rate year on year.

Revenue growth year-on-year almost exactly matched that of student weeks for adult and junior language students, at 16% and 10% respectively.

The importance of agencies was underlined by the fact that across all respondents’ business, agents recruited 85% of those students.

108 schools completing the pioneering project and 68 agencies.

Participants’ countries were spread out widely but with the UK, USA and Canada were in the top three by response rates.

Source markets that featured as very important across the broad mix of schools included Brazil, Spain and Italy.

The granular nature of the survey means that typical turnover figures per student week are available per country: there was perhaps suprising parity for most markets and adult courses, although the UK’s junior courses at US$923 per week were among the highest-grossing products.

Brazilian business was particularly well reflected in this survey, accounting for 14% of respondents but 47% of student weeks

When asked how particular issues have affected business over the last 12 months, 81% of providers said they had been negatively impacted by economic issues in source countries. A high proportion of providers had also suffered negative effects as the result of visa policy in their own country (72%), competitor school activity (65%) and school initiatives (64%).

More specific issues mentioned by respondents included media reports of violence in the destination country, ebola fears and Russia-EU relations.

As regards agency business, Brazilian business was particularly well reflected in this survey, accounting for 14% of respondents but 47% of student weeks.

Junior business accounted for 35% of total student weeks placed overall, but adult business was broadly distributed between 19-35 year olds.

Thirty-four per cent of companies surveyed said adult weeks were up year-on-year and 31% agreed on junior business performance. Again, a very similar 34% and 29% agreed that revenue had increased, year on year, for adults and juniors respectively.

It was the “no change” camp that dominated here – 39% said no change in revenues for adult business and 49% of junior business.

Currency exchange rates were cited as the biggest bête noire for agencies.

Still looking? Find by category:

Add your comment

2 Responses to ALTO’s first Language Travel Industry Survey is upbeat